Call Us Now !

Tel : +86 755 27374946

Call Us Now !

Tel : +86 755 27374946

Order Online Now !

Email : info@bichengpcb.com

Order Online Now !

Email : info@bichengpcb.com

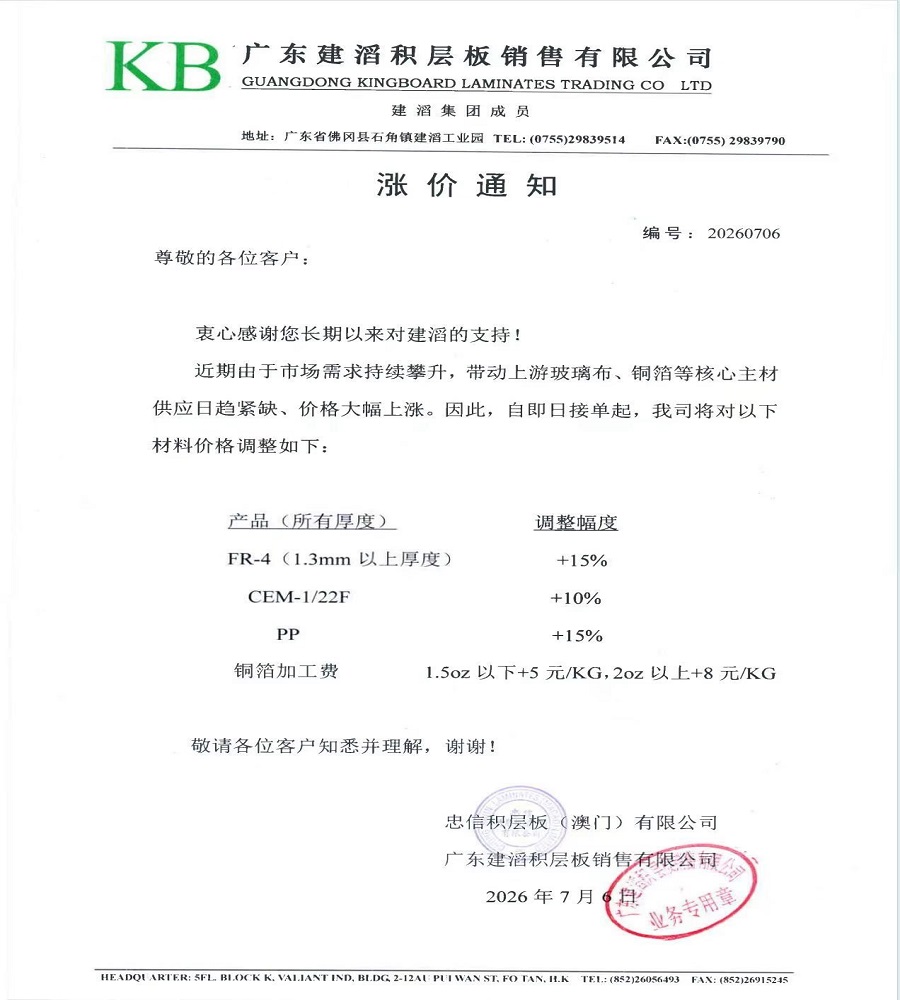

KINGBOARD ANNOUNCES PRICE INCREASE ON CCL MATERIALS AMID TIGHT SUPPLY OF UPSTREAM RAW MATERIALS July 6, 2026–Industry News Leading laminate manufacturer Kingboard Laminates has issued a formal price adjustment notice, citing persistent demand growth and severe supply constraints in upstream core materials. According to the official notification dated July 6, 2026, the company stated that rising market demand has increasingly tightened the supply of key raw materials such as glass fabric and copper foil, driving their costs significantly higher. In response, Kingboard will implement the following price revisions with immediate effect for all new orders: Product Category Adjustment FR-4 (thickness≥1.3mm) +15% CEM‑1 / 22F +10% Prepreg (PP) +15% Copper foil processing fee +5 CNY/kg for≤1.5oz; +8 CNY/kg for≥2oz The adjustment applies to all thickness grades of the affected products. The company expressed its appreciation for customer understanding and cooperation during this market-driven cost transition. This move reflects the broader pressure across the copper-clad laminate (CCL) supply chain, as strong end‑market demand–particularly in automotive electronics, AI infrastructure, and consumer devices–continues to outpace the expansion of upstream materials capacity. Industry analysts expect similar adjustments from other laminate suppliers in the coming weeks. Kingboard remains committed to stable supply and quality assurance, while closely monitoring raw material trends to support its global customer base. Source: Kingboard Laminates Trading Co., Ltd.–Official Price Notice (20260706)

EU to Abolish €150 Import Duty Exemption Threshold Starting July 1, 2026 Date: July 1, 2026 The European Union has officially announced the elimination of the€150 import duty exemption threshold, effective July 1, 2026. Under the new regulation, all parcels entering the EU will be subject to customs duties, regardless of their declared value. This marks a significant shift in EU import policy that will affect both B2B and B2C shipments. Key Changes & Requirements 1. Duty Calculation Adjustments B2C Shipments (≤ €150): Previously exempt from duties, low-value B2C parcels will now incur customs duties calculated on a per-tariff-line basis. The duty rate is set at€3 per tariff line item. B2B Shipments: Commercial shipments will continue to be taxed according to the applicable duty rate corresponding to each commodity's tariff classification. 2. Mandatory Customs Clearance Information B2B Commercial Shipments: Valid VAT number and EORI number must be provided. B2C Private Shipments: A valid IOSS (Import One-Stop Shop) number must be provided prior to shipment. ⚠️ Risk Notice: Shipments without a valid IOSS number (B2C) or VAT/EORI number (B2B) may still be dispatched, but face a very high risk of customs clearance delays, detention, return, or even destruction. All resulting losses and additional fees shall be borne by the shipper. 3. Commercial Invoice Requirements All commercial invoices must clearly indicate the trade nature as either "B2B" or "B2C" to ensure proper customs processing. 4. Upcoming Product Identifier (PID) Requirement—Effective November 1, 2026 Starting November 1, 2026, B2C parcels will additionally require the following product identification information: Trader ID—Mandatory Manufacturer ID—Mandatory Standardized Product ID—Required, where applicable These identifiers are part of the EU's broader efforts to enhance product traceability and consumer safety across the single market. What This Means for You The removal of the€150 de minimis threshold represents a major change in EU e-commerce and cross-border trade. Shippers are advised to: Review and update pricing strategies to account for the new duty costs Ensure all required identification numbers (VAT, EORI, IOSS) are registered and valid Update invoicing templates to include B2B/B2C designation Begin preparing PID compliance systems ahead of the November 1 deadline We will continue to monitor further developments and provide updates as additional guidance becomes available. Stay informed. Stay compliant.

2026 Holiday Schedule: Plan Your Orders Ahead Published: June 22, 2026 Dear Valued Customers, To help you plan your orders and shipments smoothly, we are pleased to share our official holiday schedule for the second half of 2026 and the upcoming 2027 Chinese New Year. Upcoming Public Holidays 2026–2027 Holiday Dates Duration Dragon Boat Festival Jun 19 – Jun 21, 2026 3 days Mid-Autumn Festival Sep 25 – Sep 27, 2026 3 days National Day Oct 1 – Oct 7, 2026 7 days 2027 Chinese New Year Feb 2 – Feb 13, 2027 12 days Important Notes Our holiday schedule follows the official Chinese national public holiday calendar. Please note that some holidays may require make-up working days on adjacent weekends. We will send a separate notification with detailed shipping arrangements before each holiday. The 2027 Chinese New Year holiday will last 12 days (from February 2 to February 13, resuming work on the 8th day of the first lunar month). We strongly recommend placing your orders at least 2–3 weeks in advance to avoid any delivery delays during this peak period. Shipping & Support During Holidays Our production and shipping departments will be closed on the dates listed above. For urgent inquiries, you can still reach out to your account manager via email, and we will respond as soon as we return. Orders placed shortly before a holiday may experience extended lead times. We appreciate your understanding and patience. Thank you for your continued trust and partnership. Should you have any questions about our holiday arrangements or need to adjust your order plan, please feel free to contact us at any time. —Shenzhen Bicheng Electronics Technology Co., Ltd

2026 Dragon Boat Festival Holiday Notice Dear Valued Customers, As the traditional Chinese Dragon Boat Festival of 2026 approaches, all staff of Bicheng PCB would like to extend our sincere festival wishes to you and your family. Wish you good health and all the best! In accordance with China’s official holiday schedule, our holiday arrangement is listed below: 1.Holiday Period: June 19th–June 21st, 2026, total 3 days off; 2.Back to Work: We will resume full normal work on Monday, June 22nd, 2026, including sales, engineering and production service. During the holiday, our factory will suspend production and offline office work. There will be delayed replies to emails and online messages. If you have urgent orders or prototype demands, please leave us a message, and we will prioritize your requests immediately after we return to work. We apologize for any inconvenience caused and greatly appreciate your continuous trust and support. Best regards, Shenzhen Bicheng Electronics Technology Co., Ltd June 17th, 2026

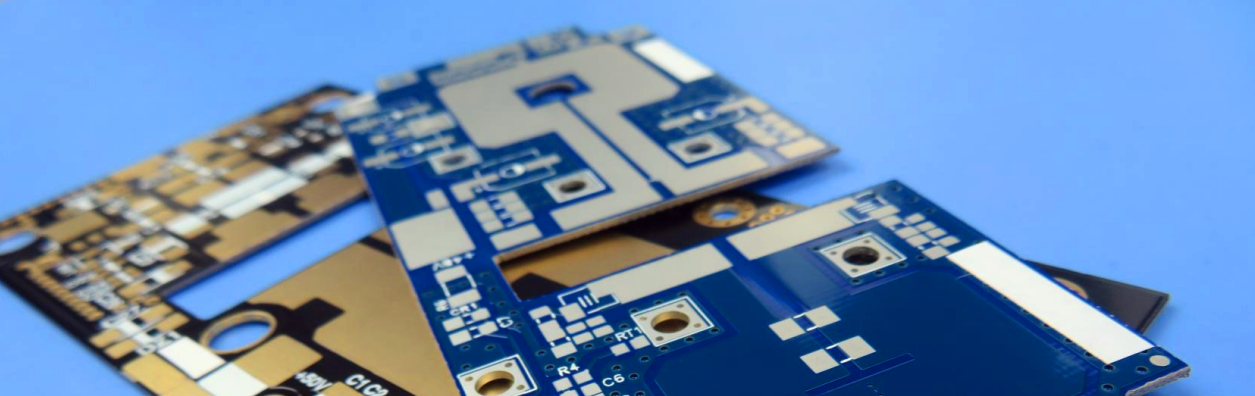

High-End Production Capacity: The Game-Changer for PCB Industry Upgrade Currently, the global PCB (Printed Circuit Board) industry is undergoing profound structural transformation. Growth in traditional low-end products is slowing down, while high-end products such as high-density interconnect (HDI) boards and high-layer count boards have become the core engines driving industry growth. On April 9, Sihui Fuji Electronics Technology Co., Ltd. (hereinafter referred to as "Sihui Fuji") unveiled a new investment plan to build high-end PCB production capacity. In addition, companies including Victory Giant Technology (HuiZhou) Co., Ltd. (hereinafter referred to as "Victory Giant"), Wus Printed Circuit (Kunshan) Co., Ltd. (hereinafter referred to as "Wus Printed Circuit"), and Avary Holding (Shenzhen) Co., Ltd. (hereinafter referred to as "Avary Holding") have also recently disclosed large-scale investment plans or full-year investment blueprints. Zheng Lei, Chief Economist at Samoyed Cloud Technology Group, said in an interview with Securities Daily: "Keeping pace with the direction of industrial transformation and upgrading and optimizing product structure are key measures for PCB enterprises to gain a foothold in the new round of industrial upgrading. Meanwhile, A-share listed companies in the industry are leveraging their advantages to increase investment in technological innovation and high-end capacity layout, which will accelerate industrial upgrading and enhance the global position of China's PCB industry." Specifically, on April 9, Sihui Fuji released its 2026 private placement plan for A-shares to specific investors. The total amount of funds raised from this private placement will not exceed 950 million yuan (inclusive). After deducting relevant issuance expenses, the net proceeds are planned to be fully used for the new construction project of 5.58 million square meters of high-reliability circuit boards per year - the 600,000 square meters per year high-layer count and HDI circuit board project (Phase I). A relevant person in charge of Sihui Fuji told Securities Daily: "To become a core supplier in the AI (Artificial Intelligence) field, the company needs to have large-scale high-end production capacity and certified stable manufacturing processes. Our current production capacity mainly meets sample and small-batch demands. The fund-raising project will enhance our ability to produce large batches of high-layer count boards and HDI boards, which is crucial for us to become a core supplier in the AI sector. This investment project is expected to further consolidate the foundation for the company's future development." In addition to Sihui Fuji,multiple PCB enterprises are increasing their investment in high-end capacity layout. On April 2, Wus Printed Circuit announced that it plans to invest approximately 6.8 billion yuan to build a printed circuit board production project and its su...

AI Demand Surge Opens Window for Domestic High-End Materials Recently, the copper clad laminate (CCL) sector has been showing sustained strength in the stock market. Data shows that since April 1, the share price of Fangbang Electronics (688020) has risen nearly 100%; the share prices of several other CCL-listed companies, including Shengyi Technology (600183) and Nanya New Material (688519), have also continued to climb. Behind the stock price increases, the rapidly growing demand for AI servers and high-speed switches is pushing the CCL industry into a supply shortage cycle. A Shanghai Securities News reporter learned that delivery times for some high-end CCL products have already been extended to more than two weeks. At the same time, key raw materials such as HVLP copper foil and low-dielectric electronic glass fabric are facing persistent supply tightness, and the supply shortage of overseas high-end materials is opening a window for domestic raw material suppliers to enter the high-end supply chain. Delivery times for high-end CCL continue to lengthen Multiple industry chain sources told reporters that compared to traditional servers, AI servers have higher requirements for signal transmission speed, loss control, and heat dissipation capability, which has led to rapidly growing demand for high-end CCL. Against this backdrop, delivery times for high-end CCL have begun to lengthen. Xiong Yiyu, a senior electronics analyst at Huachuang Securities, said in an interview that delivery times for standard CCL products remain around 7 to 10 days, while delivery times for AI-related and high-speed high-grade materials have generally been extended to more than two weeks. "Currently, delivery times for mainstream M8 high-speed materials are 3 to 4 weeks, and delivery times of more than 6 weeks are mainly concentrated on certain special grades and substrate materials," Xiong said. A board secretary of a CCL listed company told reporters that the industry's average delivery time has generally lengthened from the normal level of about 7 days to 15–20 days, and some manufacturers have extended delivery times to as long as 20–30 days. The secretary said that current orders related to high-end AI are growing rapidly, and the production processes for these products are more complex and take longer, occupying significantly more capacity than ordinary products, further exacerbating the supply shortage. In Xiong's view, the core reasons for the extended delivery times are: on the one hand, CCL manufacturers currently have relatively high overall capacity utilization; on the other hand, delivery times for upstream core raw materials such as electronic glass fabric and copper foil are also significantly lengthening, forcing CCL manufacturers to passively extend their delivery cycles. A research report from Shanxi Securities shows that the AI-driven super-cycle will remain in a ...

Categories

New Products

12-layer TG200 TU-872 SLK High-Speed FR4 1.68mm PCB with ENIG Impedance Control

12-Layer RO4350B + RO3010 3.14mm Hybrid PCB Nickel-Free EPIG Surface Finish Blind Via

8-Layer Hybrid PCB RO4003C + S1000-2M FR4 with ENIG Surface Finish Blind Via

6-Layer Isola Astra MT77 PCB with Blind Via & Resin Plug Immersion Silver Finish

2-Layer 20mil FSD1020T ENIG High-Frequency PCB with Via Resin Plugged and Capped

4-Layer F4BM265+S1000-2M Material Hyrbid PCB with Blind Via Impedance Control & ENIG

4-Layer Wangling WL-CT338 + FR4 Hybrid PCB ENIG Green Solder Mask White Silkscreen

6-layer Isola 370HR High-Tg FR-4 PCB 2μ" ENIG Impedance Controlled

6-11C Shidai Jingyuan, Fuyong, Baoan, Shenzhen, Guangdong, China 518103

6-11C Shidai Jingyuan, Fuyong, Baoan, Shenzhen, Guangdong, China 518103

For inquiries about our products or pricelist, please leave to us and we will be in touch within 24 hours.

© Copyright: 2026 Shenzhen Bicheng Electronics Technology Co., Ltd.. All Rights Reserved.

IPv6 network supported